Nepal Rastra Bank Economic Research Department, Baluwatar, Kathmandu Current Macroeconomic and Financial Situation of Nepal (Based on Three Months’ Data Ending Mid-October, 2022/23)

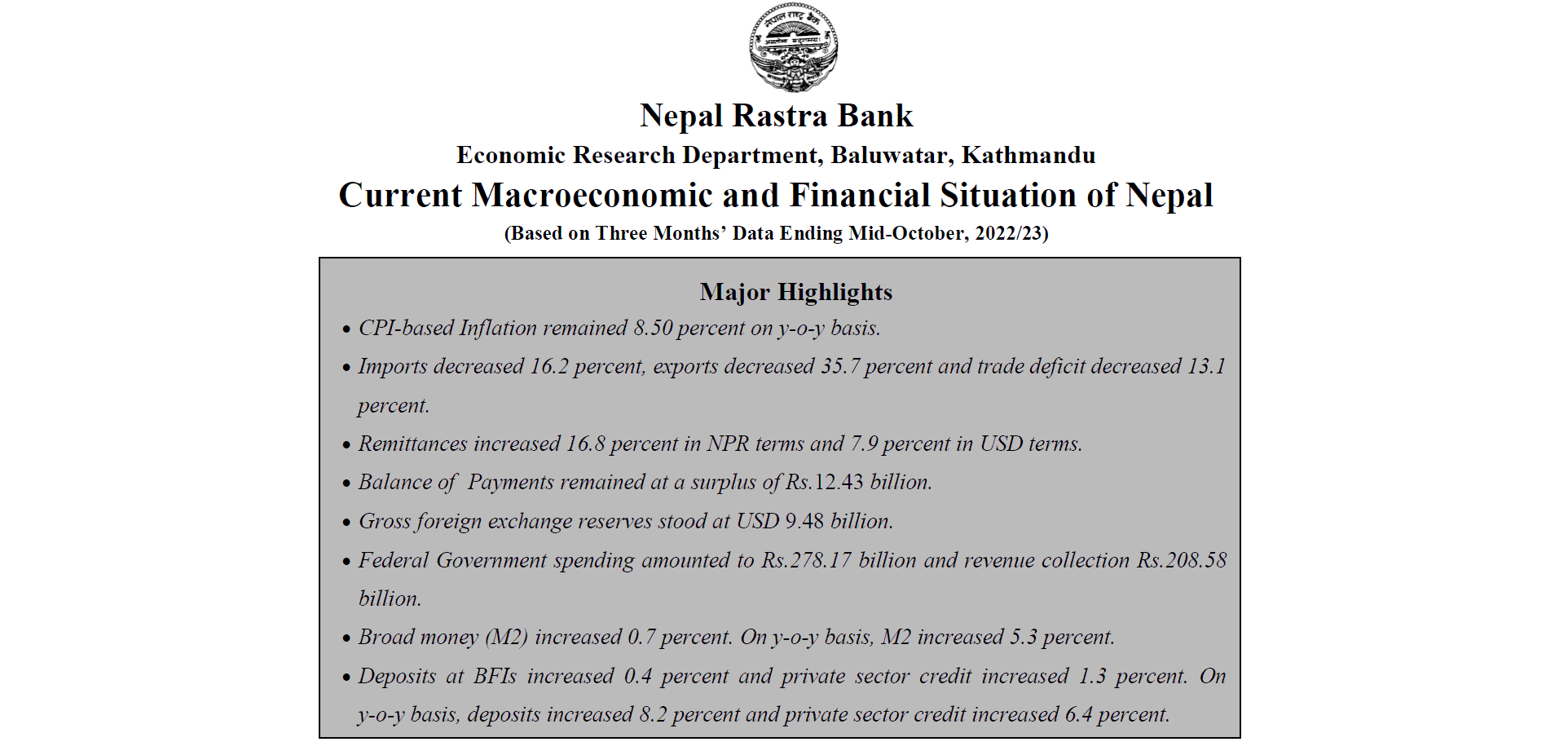

Major Highlights

- CPI-based Inflation remained 8.50 percent on y-o-y basis.

- Imports decreased 16.2 percent, exports decreased 35.7 percent and trade deficit decreased 13.1 percent.

- Remittances increased 16.8 percent in NPR terms and 7.9 percent in USD terms.

- Balance of Payments remained at a surplus of Rs.43 billion.

- Gross foreign exchange reserves stood at USD 48 billion.

- Federal Government spending amounted to Rs.278.17 billion and revenue collection Rs.208.58 billion.

- Broad money (M2) increased 0.7 percent. On y-o-y basis, M2 increased 5.3 percent.

- Deposits at BFIs increased 0.4 percent and private sector credit increased 1.3 percent. On y-o-y basis, deposits increased 8.2 percent and private sector credit increased 6.4 percent.

Inflation

Consumer Price Inflation

1. The y-o-y consumer price inflation remained at 8.50 percent in mid-October 2022 compared to 4.24 percent a year ago. Food and beverage inflation stood at 8.05 percent whereas non-food and service inflation registered 8.85 percent in the review month.

2. Under the food and beverage category, y-oy consumer price inflation of the restaurant & hotel sub-category increased 91 percent, fruit 12.06 percent, alcoholic drinks 10.24 percent, milk products & eggs 9.45 percent and tobacco products 8.44 percent.

|

Table 1: y-o-y Consumer Price Inflation (Percent) |

|||

|

Mid-Month |

|||

|

Particulars |

Sep/Oct 2021 |

Aug/Sep 2022 |

Sep/Oct 2022 |

|

Overall Inflation |

4.24 |

8.64 |

8.50 |

|

Food and Beverage |

3.63 |

8.17 |

8.05 |

|

Non-food and Service |

4.72 |

9.02 |

8.85 |

3. Under the non-food and services category, y-o-y consumer price inflation of the transportation sub-category increased by 21.15 percent, health by 10.54 percent, furnishing & household equipment by 9.45 percent, education by 8.11 percent and housing & utilities by 7.68 percent.

4. In the review month, consumer price inflation in the Kathmandu Valley, Terai, Hill and Mountain surged to 6.93 percent, 9.42 percent, 8.84 percent and 7.07 percent respectively. Inflation in these regions were 3.48 percent, 4.01 percent, 5.68 percent and 3.12 percent respectively a year ago.

Wholesale Price Inflation

5. The y-o-y wholesale price inflation increased 13.73 percent in the review month compared to 3.83 percent a year ago.

6. The y-o-y wholesale price of consumption goods, intermediate goods and capital goods increased 24 percent, 17.13 percent and 6.00 percent respectively. The wholesale price of construction materials increased 19.27 percent in the review month.

Salary and Wage Rate Index

7. The y-o-y salary and wage rate index increased by 11.59 percent in the review month compared to 4.92 percent a year ago. In the review month, salary index and wage rate index increased by 12.39 and 11.34 percent, respectively.

Consumer Price Inflation in Nepal and India

8. The y-o-y consumer price inflation in Nepal remained at 8.50 percent in mid-October 2022. Such inflation in India stood at 6.77 percent in October 2022.

External Sector

Merchandise Trade

9. During the three months of 2022/23, merchandise exports decreased 35.7 percent to Rs.41.82 billion against an increase of 109.5 percent in the same period of the previous year. Destination-wise, exports to India and China decreased 45.0 percent and 35.0 percent respectively whereas exports to other countries increased 5.0 percent. Exports of zinc sheet, particle board, woolen carpets, readymade garments, tea, among others, increased whereas exports of soyabean oil, palm oil, oil cakes, jute goods, silverware and jewelries, among others, decreased in the review period.

10. During the three months of 2022/23, merchandise imports decreased 16.2 percent to Rs.401 billion against an increase of 63.7 percent a year ago. Destination-wise, imports from India, China and other countries decreased 14.8 percent, 16.7 percent, and 19.2 percent respectively. Imports of petroleum products, chemical fertilizer, sponge iron, medicine, coal, among others, increased whereas imports of transport equipment & parts, silver, telecommunication equipments and parts, crude soyabean oil, M.S. wire rod, bars, coils & others, among others, decreased in the review period.

11. Based on customs points, exports from Dry Port, Jaleshwor, Kailali, Krishnanagar, Mechi and Tribhuwan Airport Customs Offices increased whereas exports from all the other major customs points decreased in the review period. On the import side, imports from Dry Port, Jaleshwor and Tatopani Customs Offices increased whereas imports from all the other major customs points decreased in the review period.

12. Total trade deficit decreased 13.1 percent to Rs.359.18 billion during the three months of 2022/23. Such a deficit had increased 58.3 percent in the corresponding period of the previous year. The export-import ratio decreased to 10.4 percent in the review period from 13.6 percent in the corresponding period of the previous year.

13. During the three months of 2022/23, merchandise imports from India by paying convertible foreign currency amounted Rs.34.59 billion. Such amount was Rs.54.17 billion in the same period of the previous year.

Composition of Foreign Trade

14. As per the Broad Economic Categories (BEC), the intermediate and final consumption goods accounted for 57.0 percent and 43.0 percent of the total exports respectively, whereas the ratio of capital goods in total exports remained negligible at 0.03 percent in the review period. In the same period of the previous year, the ratio of intermediate, capital and final consumption goods remained 41.8 percent, 0.03 percent and 58.2 percent of total exports respectively.

15. On the imports side, the share of intermediate goods remained 53.2 percent, capital goods 8.3 percent and final consumption goods remained 38.5 percent in the review period. Such ratios were 53.0 percent, 11.0 percent and 36.0 percent respectively in the same period of the previous year. Export-Import Price Index

16. The y-o-y unit value export price index, based on customs data, increased 4.1 percent and the import price index increased 12.4 percent in the third month of 2022/23. The terms of trade (ToT) index decreased 7.4 percent in the review month compared to a decrease of 3.1 percent a year ago.

Services

17. Net services income remained at a deficit of Rs.21.70 billion in the review period compared to a deficit of Rs.23.34 billion in the same period of the previous year.

18. Under the service account, travel income increased 110.4 percent to Rs.11.41 billion in the review period which was Rs.5.42 billion in the same period of the previous year.

19. Under the service account, travel payments increased 62.3 percent to Rs.26.04 billion, including Rs.17.89 billion for education. Such payments were Rs.16.04 billion and Rs.8.92 billion respectively in the same period of the previous year. Remittances

20. Remittance inflows increased 16.8 percent to Rs.281.05 billion in the review period against a decrease of 7.1 percent in the same period of the previous year. In the US Dollar terms, remittance inflows increased 7.9 percent to 2.19 billion in the review period against a decrease of 7.1 percent in the same period of the previous year.

21. The number of Nepali workers taking new approval (institutional and individual) for foreign employment increased 123.1 percent to 147,932 in the review period. Likewise, the number of Nepali workers taking renew entry approval for foreign employment increased 66.2 percent to 57,861 in the review period. It had increased by 219.7 percent in the same period of the previous year.

22. Net transfer increased 17.1 percent to Rs.310.43 billion in the review period. Such a transfer had decreased 7.6 percent in the same period of the previous year. Current Account and Balance of Payments

23. The current account remained at a deficit of Rs.34.28 billion in the review period compared to a deficit of Rs.149.81 billion in the same period of the previous year. In the US Dollar terms, the current account registered a deficit of 269.5 million in the review period compared to deficit of 1.26 billion in the same period last year.

24. In the review period, capital transfer increased 34.8 percent to Rs.2.59 billion and net foreign direct investment (FDI) remained Rs.79.6 million. In the same period of the previous year, capital transfer and net FDI amounted to Rs.1.92 billion and Rs.5.07 billion respectively.

25. Balance of Payments (BOP) remained at a surplus of Rs.12.43 billion in the review period compared to a deficit of Rs.87.71 billion in the same period of the previous year. In US Dollar terms, the BOP remained at a surplus of 91.8 million in the review period compared to a deficit of 741.2 million in the same period of the previous year. Foreign Exchange Reserves

26. Gross foreign exchange reserves increased 5 percent to Rs.1246.22 billion in mid-October 2022 from Rs.1215.80 billion in mid-July 2022. In US dollar terms, the gross foreign exchange reserves decreased 0.6 percent to 9.48 billion in mid-October 2022 from 9.54 billion in mid-July 2022.

27. Of the total foreign exchange reserves, reserves held by NRB increased 4.3 percent to Rs.1101.60 billion in mid-October 2022 from Rs.1056.39 billion in mid-July 2022. Reserves held by banks and financial institutions (except NRB) decreased 9.3 percent to Rs.144.62 billion in mid-October 2022 from Rs.159.41 billion in mid-July 2022. The share of Indian currency in total reserves stood at 23.8 percent in mid-October 2022.

Foreign Exchange Adequacy Indicators

28. Based on the imports of three months of 2022/23, the foreign exchange reserves of the banking sector is sufficient to cover the prospective merchandise imports of 9.6 months, and merchandise and services imports of 8.3 months. The ratio of reserves-to-GDP, reserves-to-imports and reserves-to-M2 stood at 25.7 percent, 69.5 percent and 22.5 percent respectively in mid-October 2022. Such ratios were 25.1 percent, 57.8 percent and 22.1 percent respectively in mid-July 2022. Price of Oil and Gold

29. The price of oil (Crude Oil Brent) in the international market increased 7.5 percent to US dollar 91.04 per barrel in mid-October 2022 from US dollar 84.67 per barrel a year ago. The price of gold decreased 6.1 percent to US dollar 1664.75 per ounce in mid-October 2022 from US dollar 1772.65 per ounce a year ago. Exchange Rate

30. Nepalese currency vis-à-vis the US dollar depreciated 3.01 percent in mid-October 2022 from midJuly 2022. It had depreciated 0.90 percent in the same period of the previous year. The buying exchange rate per US dollar stood at Rs.131.47 in mid-October 2022 compared to Rs.127.51 in mid-July 2022.

Fiscal Situation

Federal Government

Expenditure and Revenue

|

Table 2: Government Expenditure and Revenue (Three Months) |

||||

|

Particulars |

Amount (Rs. in Billion) |

Percentage Change |

||

|

2021/22 |

2022/23 |

2021/22 |

2022/23 |

|

|

Total Expenditure |

234.52 |

278.17 |

16.6 |

18.6 |

|

Recurrent Expenditure |

186.52 |

223.75 |

2.1 |

20.0 |

|

Capital Expenditure |

14.89 |

19.68 |

-1.1 |

32.2 |

|

Financial Management |

33.11 |

34.73 |

871.0 |

4.9 |

|

Total Revenue |

255.04 |

208.58 |

48.0 |

-18.2 |

|

Tax Revenue |

229.08 |

189.38 |

40.2 |

-17.3 |

|

Non-Tax Revenue |

25.96 |

19.20 |

190.4 |

-26.0 |

31. During the three months of 2022/23, total expenditure of the federal government according to data of Financial Comptroller General Office (FCGO), Ministry of Finance, stood at Rs.278.17 billion. The recurrent expenditure, capital expenditure and financial expenditure amounted to Rs. 223.75 billion, Rs.19.68 billion and Source: Financial Comptroller General Office Rs.34.73 billion respectively in the review period.

32. In the review period, revenue mobilization (including the amount to be transferred to provincial and local governments) stood at Rs.208.58 billion. The tax revenue and non tax revenue amounted Rs.189.38 billion and Rs.19.20 billion respectively in the review period (Table 2). Cash Balance

33. Balance at various accounts of the GoN maintained with NRB remained Rs.195.62 billion (including Provincial government and Local Authorities Account) in mid-October 2022. Such a balance was Rs.227.69 billion in mid-July 2022. Provincial Government

34. In the review period, total resource mobilization of provincial governments remained Rs.34.30 billion. The federal government transferred Rs.23.66 billion as grants and revenue from federal divisible fund to provincial governments and the provincial governments mobilized Rs.10.64 billion in terms of revenue and other receipts in the review period. In the review period, total expenditure of provincial governments stood at Rs.20.99 billion.

Monetary Situation

Money Supply

35. Broad money (M2) increased 0.7 percent in the review period compared to an increase of 2.2 percent in the corresponding period of the previous year. On y-o-y basis, M2 expanded 5.3 percent in mid-October 2022.

36. The net foreign assets (NFA, after adjusting foreign exchange valuation gain/loss) increased Rs.12.43 billion (1.1 percent) in the review period in contrast to a decrease of Rs. 87.71 billion (6.6 percent) in the corresponding period of the previous year.

37. Reserve money increased 6.3 percent in the review period in contrast to a decrease of 2.8 percent in the corresponding period of the previous year. On y-o-y basis, reserve money decreased 3.1 percent in mid-October 2022. Domestic Credit

38. Domestic credit increased 1.5 percent in the review period compared to an increase of 5.1 percent in the corresponding period of the previous year. On y-o-y basis, domestic credit increased 10.5 percent in mid-October 2022.

39Monetary Sector's claims on the private sector increased 1.6 percent in the review period compared to an increase of 7.8 percent in the corresponding period of the previous year. On y-o-y basis, such claims increased 6.8 percent in mid-October 2022. Deposit Mobilization

|

Table 3: Deposits at Banks and Financial Institutions (Percentage Share) |

||||

|

Deposits |

Mid-July |

Mid-October |

||

|

2021 |

2022 |

2021 |

2022 |

|

|

Demand |

10.4 |

8.9 |

7.7 |

7.6 |

|

Saving |

34.2 |

27.6 |

34.4 |

26.7 |

|

Fixed |

47.0 |

55.8 |

50.4 |

59.0 |

|

Other |

8.4 |

7.7 |

7.5 |

6.7 |

40. Deposits at Banks and Financial Institutions (BFIs) increased 0.4 percent in the review period compared to an increase of 1.2 percent in the corresponding period of the previous year. On y-oy basis, deposits at BFIs expanded 8.2 percent in mid-October 2022.

41. The share of demand, saving, and fixed deposits in total deposits stands at 7.6 percent, 26.7 percent and 59.0 percent respectively in mid-October 2022. Such shares were 7.7 percent, 34.4 percent and 50.4 percent respectively a year ago.

42. The share of institutional deposits in total deposit of BFIs stands at 37.0 percent in mid-October 2022. Such a share was 40.5 percent in mid-October 2021.

Credit Disbursement

43. Private sector credit from BFIs increased 1.3 percent in the review period compared to an increase of 7.7 percent in the corresponding period of previous year. On y-o-y basis, credit to the private sector from BFIs increased 6.4 percent in mid-October 2022.

44. The shares of private sector credit from BFIs to non-financial corporation and household stand at 63.9 percent and 36.1 percent respectively in mid-October 2022. Such shares were 64.2 percent and 35.8 percent a year ago.

45. In the review period, private sector credit from commercial banks, development banks and finance companies increased 1.2 percent, 2.6 percent and 0.3 percent respectively.

46. In the review period, out of the total outstanding credit of the BFIs, 66.7 percent is against the collateral of land and building and 12.2 percent against the collateral of current assets (such as agricultural and non-agricultural products). Such ratios were 66.6 percent and 12.3 percent respectively a year ago.

47. In the review period, outstanding loan of BFIs to industrial production sector increased 5.6 percent, service industry sector 3.9 percent, transportation, communication and public sector 2.8 percent, wholesale & retail sector 2.2 percent, construction sector 1.7 percent and agriculture sector 0.8 percent.

48. In the review period, term loan extended by BFIs increased 4.2 percent, overdraft 4.8 percent, trust receipt (import) loan 2.8 percent, demand and working capital loan 3.0 percent, real estate loan (including residential personal home loan) 2.7 percent whereas hire purchase loan and margin nature loan decreased by 1.5 percent and 5.2 percent respectively. Liquidity Management

49. In the review period, NRB injected Rs.2355.09 billion liquidity, of which Rs.188.66 billion was through repo, Rs.43.70 billion through outright purchase auction and Rs.2122.73 billion through standing liquidity facility (SLF). In the corresponding period of the previous year 948.17 billion net amount of liquidity was injected through various instruments of open market operations.

50. In the review period, NRB injected liquidity of Rs.154.04 billion through the net purchase of USD 1200 million from foreign exchange market. Liquidity of Rs.29.73 billion was injected through the net sale of USD 247.6 million in the corresponding period of the previous year.

51. The NRB purchased Indian currency (INR) equivalent to Rs.130.41 billion through the sale of USD 1.02 billion in the review period. INR equivalent to Rs.111.53 billion was purchased through the sale of USD 940 million in the corresponding period of previous year. Refinance, Concessional Loan and Business Continuity Loan

52. The outstanding amount of refinance provided by NRB remained Rs.105.47 billion in mid-October 2022.

53. As of mid-October 2022, the outstanding concessional loan is Rs.210.47 billion extended to 147,642 borrowers. Of which, Rs.138.21 billion has been extended to 60,061 borrowers for selected commercial agriculture and livestock businesses. Likewise, 68.69 billion loan has been extended to 84,750 women entrepreneurs. Total 2,831 borrowers have availed Rs.3.57 billion concessional loan in other sectors.

54. Business continuity loan has been extended to the Covid-19 affected tourism, cottage, small and medium industries for payment of salaries to workers and employees in line with 'Business Continuity Loan Procedure, 2020'. The outstanding loan extended under this provision is Rs. 903.4 million as of mid-October 2022. Inter-bank Transaction

55. In the review period, BFIs' interbank transactions amounted Rs.941.61 billion including Rs.856.02 billion inter-bank transactions among commercial banks and Rs.85.58 billion among other financial institutions (excluding transactions among commercial banks). In the corresponding period of the previous year, such transactions was Rs.919.89 billion including Rs.797.28 billion among commercial banks and Rs.122.61 billion among other financial institutions (excluding transactions among commercial banks). Interest Rates

|

Table 4: Weighted Average interest rate (percent) |

||

|

Types |

Mid-October 2021 |

Mid-October 2022 |

|

91-days treasury bills rate |

4.86 |

10.14 |

|

Inter-bank rate |

4.95 |

8.50 |

|

Base rate |

7.57 |

10.34 |

|

Deposit rate |

5.43 |

8.16 |

|

Lending rate |

8.69 |

12.19 |

56. The weighted average 91-days treasury bills rate remained at 10.14 percent in the third month of 2022/23, which was 86 percent in the corresponding month a year ago. The weighted average inter-bank transaction rate among commercial banks, which was 4.95 percent a year ago, increased to 8.50 percent in the review month. The average inter-bank rate of BFIs which is considered as operating target of monetary policy, stood 8.51 percent in the review month. Such a rate was 4.95 percent a year ago.

57. The average base rate of commercial banks increased to 10.34 percent in the third month of 2022/23 from 7.57 percent a year ago. Weighted average deposit rate and lending rate of commercial banks stood at 8.16 percent and 12.19 percent respectively in the review month. Such rates were 5.43 percent and 8.69 percent respectively a year ago. Merger and Acquisition

58. After introduction of merger and acquisition policy aimed at strengthening financial stability, the number of BFIs involved in this process reached 247 as of mid-October 2022. Out of which, the license of 179 BFIs was revoked thereby forming 68 BFIs. Financial Access

59. Of the total 753 local levels, commercial banks extended their branches at 752 levels as of mid October 2022. The number of local levels having commercial bank branches was 750 a year ago.

60. The total number of BFIs licensed by NRB remained 125 in mid-October 2022 (Table 5). As of mid-October 2022, 26 commercial banks, 17 development banks, 17 finance companies, 64 microfinance financial institutions and 1 infrastructure development bank are in operation. The number of BFIs branches reached 11,609 in mid-October 2022 from 11,528 in mid-July 2022 (Table 5).

|

Table 5: Number of BFIs and their Branches* |

|

|||||

|

Bank and Financial Institutions |

Number of BFIs |

|

Branches of BFIs |

|||

|

mid-July 2021 |

mid- July 2022 |

mid-October 2022 |

mid-July 2021 |

mid-July 2022 |

mid-October 2022 |

|

|

Commercial Banks |

27 |

26 |

26 |

4753 |

5009 |

5074 |

|

Development Banks |

18 |

17 |

17 |

1023 |

1118 |

1121 |

|

Finance Companies |

17 |

17 |

17 |

222 |

267 |

274 |

|

Microfinance Financial Institutions |

70 |

65 |

64 |

4685 |

5134 |

5140 |

|

Infrastructure Development Bank |

1 |

1 |

1 |

- |

- |

- |

|

Total |

133 |

126 |

125 |

10683 |

11528 |

11609 |

*Updated information is available at http://emap.nrb.org.np/

Electronic Payment Transaction

61. Electronic payment transaction has increased significantly due to the development of payment infrastructure, policy of encouraging electronic payments and gradual adoption of electronic payment instruments (Table 59).

Capital Market

62. NEPSE index stood 1858.3 in midOctober 2022 compared to 2657 in midOctober 2021.

63. Stock market capitalization in midOctober 2022 stood Rs.2672.79 billion compared to Rs.3719.72 billion in mid October 2021.

64. Number of companies listed at NEPSE reached 242 in mid-October 2022, out of which 146 are Bank and Financial Institutions (BFIs) and insurance companies, 59 hydropower companies, 19 manufacturing and processing industries, 6 investment companies, 5 hotels, 4 trading companies and 3 others. The number of companies listed at NEPSE was 222 in mid-October

65. Share of BFIs and insurance companies in stock market capitalization is 68.6 percent. Such a share for hydropower companies is 10.5 percent, investment companies 6.4 percent, manufacturing and processing industries 4.4 percent, hotels 1.7 percent, trading companies 0.4 percent and the share of other companies is 8.1 percent.

66. The paid-up value of 6.82 billion shares listed at NEPSE stood Rs.672.69 billion in mid-October

67. Securities worth Rs.80.78 billion were listed at NEPSE during the three months of 2022/23. Such securities comprise govt. bond worth Rs.35 billion, debenture worth Rs.25.44 billion, bonus shares worth Rs.9.29 billion, ordinary share worth Rs.6.57 billion, mutual fund worth Rs.3.27 billion and right share worth Rs.1.21 billion.

68. Securities Board of Nepal approved the total public issuance of securities worth Rs.9.39 billion which includes debenture worth Rs.4.24 billion, mutual fund worth Rs.3.15 billion, ordinary share worth Rs.1.05 billion and right share worth Rs. 954 million in the review period.